Economic Corridor Development in Malaysia

Development of Economic Corridors in Malaysia

Associate Professor Harlina Suzana Jaafar, Ph.D.

University Teknologi Mara, Puncak Alam Campus, Malaysia

1. Introduction

Since gaining independence in 1957, Malaysia has diversified its economy from an agriculture and commodity-based one to hosting robust manufacturing and service sectors, becoming a key exporter of electrical appliances, parts, and components.

With a population of over 34 million, Malaysia is an upper middle-income economy. It is a leading open economy, with a trade to gross domestic product (GDP) ratio averaging over 130% since 2010. Openness to trade and investment has been instrumental in employment creation and income growth, with about 40% of jobs in Malaysia linked to export activities. After the Asian financial crisis of 1997-1998, Malaysia’s economy has been on an upward trajectory, averaging growth of 5.4% since 2010. By 2024, it is expected to achieve its transition from an upper middle-income to high-income economy (The World Bank, 2022). This is due to a growing affluent middle class significantly influencing consumer and business demand for quality goods and services, a developed infrastructure, an English-speaking business environment, a well-established legal framework, and the ability to repatriate capital and profits. Malaysia is generally considered an easy and cost-competitive market for business (East Asia Forum, 2024). Despite the impact of the Coronavirus disease 2019 (Covid-19) pandemic, the Malaysian economy has proved its resilience, achieving a growth rate of 3.3 per cent in the third quarter of 2023. This was a reasonable rate given the moderate global environment, but it was only marginally larger than the 2.9 per cent achieved for the second quarter of 2023 (East Asia Forum, 2024).

To assist the smooth development of the national economy, the government has introduced a Malaysia Five Year Plan (RMK) since 1965 as guidelines for economic development and growth implementation. RMK is a medium-term quinquennial plan comprising a comprehensive outline of government development policies and strategies (Alhabshi, 2011). Currently, Malaysia is in the progress phase of the twelfth national plan for 2020 to 2025.

In the Ninth Malaysia Plan, economic corridors were introduced in 2006 to serve as strategic instruments for fostering economic growth by attracting foreign investments into the manufacturing sector. Spanning approximately 70 percent of Malaysia’s landmass, these corridors have drawn investments from domestic and multinational giants, including Petronas, Genting Group, Siemens, Temasek Holdings, Shell, and Samsung. Since their inception, the economic corridors have accumulated an estimated investment of over 700 billion ringgit (US$150 billion). The corridors aim to become hubs for high-tech industries like semiconductors and establish the country as a key link in global supply chains (ASEAN Briefing Magazine, 2023). Development of these corridors is monitored by federal government agencies.

Thus, this chapter presents development economic corridors (EC) in Malaysia, aspects of its challenges, and strategies to overcome them.

2. Economic Corridor Development in Malaysia

When Malaysia gained independence from Britain in 1957, there was a development gap between different areas of Peninsular Malaysia. Regions along the West Coast from Penang to Johor Bahru were economically developed before the East Coast. The Titiwangsa Range bisecting Peninsular Malaysia and distances to port facilities prevent resource exploitation in the East Coast region. In 1985, Selangor, Penang, and the Federal Territory of Kuala Lumpur in the West Coast region were the most developed states with per capita GDP above the Peninsular Malaysia average. The poorest states in East Malaysia mostly involved the Malay population (Ngah, 2011). This situation has caused disparities among different states in Peninsular Malaysia, as reflected in service levels, income, social welfare, basic utility provision, health facilities, and poverty rates.

The association of race with economic indicators such as income, employment, economic sector, and corporate ownership was also significant. Malays are predominantly involved in the primary sectors (agriculture, forestry, and fishing), while the Chinese dominate the manufacturing, commercial, mining and construction sectors and the Indian population is distributed throughout all sectors (Ngah, 2011, Mohamad, 1987). Many dimensions of disparity have influenced political instability which led to race riots in May 1969. Alliance party leaders formulated the New Economic Policy (NEP) as a long-term solution to overcome the problem of inequalities.

Under the NEP (1970-1990), regional development planning was seen as a method for eradicating poverty and restructuring society in social, economic and spatial components. Among strategies adopted by the Malaysian government to solve uneven regional development were developing new land in frontier regions as well as existing or in-situ rural settlements; dispersing industrial activities to less developed regions; and creating new growth centres or townships in rural areas (see Alden and Awang, 1985; Mat 1983).

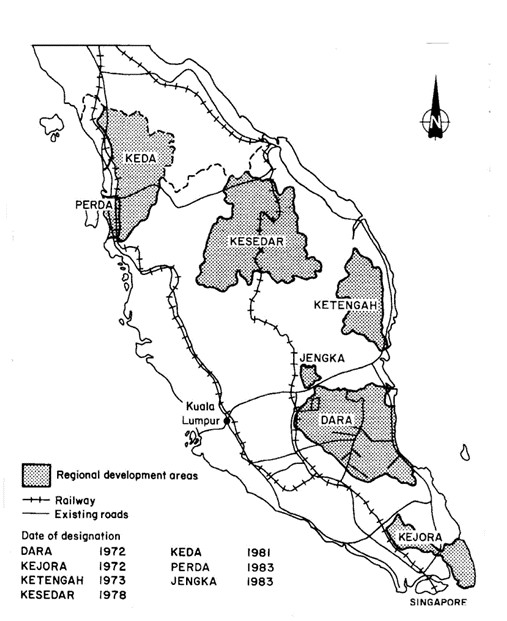

Several statutory regional development authorities were established to implement the development strategy in the resource frontier areas, mainly virgin forest in less-developed parts of Peninsular Malaysia, such as Southeast Pahang, Southeast Johor, Southern Kelantan and Central Terengganu (refer Figure 1). Most RDAs, particularly those related to development of new towns, were established in the 1970s, soon after the NEP was launched:

- Pahang Tenggara Development Authority (DARA)

- Johor Tenggara Development Authority (KETENGAH)

- Jengka Regional Development Authority (JENGKA)

- South Kelantan Development Authority (KESEDAR)

- Penang Regional Development Authority (PERDA)

- Kedah Regional Development Authority (KEDA)

When NEP ended in 1990, the government dissolved RDAs by stages to favour private-led growth. Then the government launched a second outline perspective plan, the New Development Policy (NDP). NDP (1991-2000) strategies had four dimensions: eradicating extreme poverty; rapidly developing an active Bumiputera Commercial and Industrial community; relying more on the private sector; and stressing human resource development as a growth engine. To reduce the burden of government, many state agencies providing public services were privatized: postal delivery, electricity, water supply, telecommunications, ports, and airports. New mega projects were initiated by the government in the core region of Kuala Lumpur Conurbation to boost the growth of high-tech industries and attract global investors to the services sector. Among the projects were the Kuala Lumpur International Airport (KLIA), Kuala Lumpur Commercial Centre (KLCC), Multi-Media Super Corridors and other infrastructures to attract information and communication technology (ICT) companies, develop Cyberjaya, and build a new federal administrative centre of Putrajaya.

Figure 1 Distribution of Regional Development Authorities in Malaysia (1972-1983)

Development of the core region of Kuala Lumpur Conurbation, covering most of Selangor and the Federal Territory of Kuala Lumpur, was planned to spill over to adjacent states such as Negeri Sembilan, Melaka and the southern part of Perak at the border of Selangor State. Consequently, high population growth in a few core areas with major migration flows to Kuala Lumpur Conurbation, Johor Bahru, and Penang between 1990 to 2000 resulted in more traffic congestion, flash floods due to upland area development, pollution, and pressure on infrastructure including water supply and sewage disposal. This led to the establishment of five regional economic corridors (REC).

2.1. National Economic Corridor Development

Corridor development was launched in 2006 under the Ninth Malaysia Plan (2006– 2010), (Government of Malaysia, 2006: 28) as a vehicle for achieving balanced growth due to increasing urban-rural income disparities in the 1990s.

It is expected that the corridor development will reduce regional imbalances and bring equitable growth, investment, and employment opportunities to all regions of Malaysia to create comprehensive and widespread, more coordinated and integrated economic growth. Forecasts suggested that income generation accompany accelerated poverty eradication, societal restructuring and overall wealth creation. To facilitate and expedite implementation of programs, regional corridor authorities were established. Corridor development will be private sector driven; the governmental role is to provide a conducive environment for attracting private sector participation through a competitive incentive package and creating one-stop centres to enhance service delivery and promote investment. The five corridors cover almost 70 percent of the nation’s landmass (see Figure 2).

Figure 2 Regional Economic Corridors in Malaysia

Combining infrastructure and legal and regulatory framework, the investment corridors will promote free trade and improve cross-border connectivity. Distinct incentives provided by each investment corridor support this business ecosystem. This has resulted in development of diverse sectors such as oil and gas, manufacturing, agriculture, logistics, tourism, and biotechnology:

- Northern Corridor Economic Region (NCER)

Figure 3 The Northern Corridor Economic Region (NCER)

- Iskandar Malaysia (IM)

Figure 4 Iskandar Malaysia (IM)

- • East Coast Economic Region (ECER)

Figure 5 East Coast Economic Region (ECER)

- • Sabah Development Corridor (SDC)

Figure 6 Sabah Development Corridor

- • Sarawak Corridor Renewable Energy (SCORE)

Figure 7 Sarawak Corridor Renewable Energy (SCORE)

Table 1 National Economic Corridors in Malaysia

| Iskandar Malaysia (IM) | Northern Corridor Economic Region (NCER) | East Coast Economic Region (ECER) | Sabah Development Corridor (SDC) | Sarawak Corridor of Renewable Energy (SCORE) | |

| Establishment | 2006 | 2008 | 25 February 2008. | 26 February 2009 | 2006 |

| Development period | 2006-2025 | 2007-2025 | 2007-2020 | 2008-2025 | 2008-2030 |

| Vision | A strong, sustainable metropolis of international standing | World-class economic region by 2025 | A developed region-distinctive and competitive dynamic | Harnessing unity in diversity of wealth creation and social wellbeing. | Developed and industrialised state |

| Areas of Coverage | 2,217 sq. km (District of Johor Bahru and partial district of Pontian-Mukim Jeram Batu, Mukim Sungai Karang, Mukim Serkat and Pulau Kukup). In 2019, the land area doubled in size to 4749sq km. | 17,816 sq. km extended to 32,404 sq. km (Penang, Kedah, Perlis and Northern Perak districts of Hulu Perak, Kerian, Kuala Kangsar and Larut Matang-Selama) | 66,736 sq. km (Pahang, Kelantan, Terengganu and district of Mersing, Johor) | 73,997 sq. km (entire Sabah) | 70,708 sq. km extended to 100,000 sq.km (about 80% of Sarawak) (Tanjung Manis-Samalaju and hinterland) |

| Focus sector/ Industry | Tourism, education, healthcare, finance, creative industry, food and agro-processing, petrochemicals and oleo-chemicals, electrical and electronics | (1) High-value Manufacturing Aerospace, electrical and electronics (E&E), machinery and equipment (M&E), fast moving consumer goods (FMCG), rubber products, automotive and medical devices. (2) Advanced Services Tourism, Logistics and connectivity, digital economy and education. (3) Modern Agribusiness Paddy, cash crops, fisheries and livestock. | Agriculture, Education, Manufacturing, Oil, gas & petrochemical, and Tourism | Agriculture, Environment, Human Capital, Infrastructure, manufacturing and Tourism, ICT, Biotech, and Nanotechnology | 10 high-impact priority industries: Palm oil, aquaculture, timber, aluminium, steel, marine engineering, tourism, livestock, oil and gas, and solar gas |

| Corridor Authority | Iskandar Region Development Authority (IRDA) | Northern Corridor Implementation Authority (NCIA) | East Coast Economic Region Development Council (ECERDC) | Sabah Economic Development and Investment Authority (SEDIA) | Regional Corridor Development Authority (RECODA) |

| Act | Act 664 Iskandar Regional Development Authority Act 2007 | Act 687 Northern Corridor Implementation Authority Act 2008 | Act 688 The East Coast Economic Region Development Council Act 2008 | Sabah Economic Development and Investment Authority Enactment 2009 | RECODA Ordinance 2006. |

| Expected Employment (million) | 1.4 | 3.16 | 1.9 | 2.1 | 3.0 |

| Achievement Employment (million) | 1.3 million anticipated in 2025 | In 2020, NCER created over 150,000 jobs. | In 2016, 120,000 new jobs created | In 2020, 196491 jobs were created. By 2025, 900,000 new jobs targeted | 343,368 jobs created |

| Expected Initial Investment (RM billion) | 382 | 178 | 112 | 113 | 334 |

| UPDATED: Targeted Investments (RM billion) | As of June 2020, IM has accumulated 332 billion ringgit (US$80.25 billion) 194 billion ringgit (US$46.8 billion) in total cumulative realized investments. Of these, 40% were foreign investments. | In 2020, NCIA attracted 120 billion ringgit (US$29 billion) in cumulative investments, which surpassed its investment targets for 2020, attracting 15.6 billion ringgit (US$3.7 billion) above the target of seven billion ringgit (US$1.6 billion), despite the Covid-19 pandemic. | Between 2007-2019 45% domestic investment 55% Foreign Direct Investment | In 2020, RM30.36 billion realised investments in diverse economic activities: agriculture, tourism, energy, manufacturing, and logistics. | By 2030, In 2020, secured RM167.50 billion in realised investment, mainly in the manufacturing and heavy industries as well as palm oil and energy sectors, which created |

| Major ports | Johor Port Port of Tanjung Pelepas | Penang Port | Port of Kuantan | Port of Bintulu | Bintulu, Kuching, Miri, Samalaju, Rajang and Tanjung Manis Ports. |

| International airports | Senai International airport | Penang International airport Langkawi International Airport | None | Kota Kinabalu International Airport | Kuching International airport |

2.2. Bilateral Economic Corridor

Johor-Singapore Special Economic Zone

By the end of 2024, Singapore and Malaysia will partner to create a special economic zone (SEZ) in Johor, Malaysia (JS-SEZ) next to the Singaporean border. The joint effort is designed to improve business connections and connectivity between the two nations, as the region combats a global economic slowdown. The JS-SEZ is expected to attract more multinational firms into Johor as part of a risk-management strategy caused by U.S.-China trade tensions (ASEAN Briefing, 2024).

The planned SEZ seeks to enhance the movement of goods and people across the Johor-Singapore Causeway, while strengthening the overall IM and Singapore ecosystem. The JS-SEZ is set to be established in Iskandar Malaysia (formerly the Iskandar Development Region and South Johor Economic Region), with government promotion as an attractive investment destination for boosting the electronics, healthcare, and financial industries as well as business-related services.

In 2022, Singapore and Malaysia ranked as each other’s second-largest trading partners, as their bilateral trade volume reached US$83.53 billion. Additionally, during the same year, Singapore was among Malaysia’s primary sources of foreign direct investment (FDI), contributing 8.3 percent to Malaysia’s total investments. The success of the JS-SEZ, will depend on incentive types issued by the economic zone and how these policies, tax breaks, and bonded warehouses are implemented (ASEAN Briefing, 2024).

2.3. Regional Economic Corridor Development

IMT-GT is a subregional cooperation initiative formed by the governments of Indonesia, Malaysia, and Thailand in 1993 to accelerate economic transformation in their least-developed provinces and states. The project seeks to promote welfare and economic growth for inhabitants of areas covered by the IMT-GT.

It is expected to spur development in selected regions: southern Thailand, several states in Malaysia (including NCER region) and areas in Sumatra, Indonesia. To stimulate cross-border economic integration between regions, six priority areas have been identified: agriculture and fisheries; infrastructure development; trade; tourism; human resource development; and professional services.

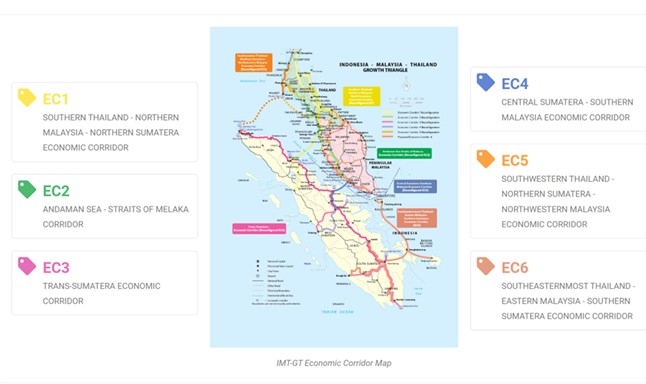

There are five priority economic corridors in IMT-GT (see Figure 8). Each has its own unique characteristics as defined by geographic location and comparative advantages. The IMT-GT corridors therefore represent a convergence of regional economic integration and inclusive growth.

Figure 8 Regional Economic Corridors in IMT-GT

Malaysia is involved in four regional EC projects under IMT-GT:

- EC 1: The Extended Songkhla-Penang-Medan Economic Corridor

EC1 consists of three main sections: two overland routes and a maritime route. The two overland routes connect i) the Southern Thailand provinces of Nakhon Si Thammarat, Phatthalung, and Pattani with international gateway portsin Songkhla, Yala, and Narathiwat; ii) an overland route from Songkhla to Penang; and iii) a maritime route linking Penang to Medan, the capital of North Sumatra, across the Strait of Malacca. In North Sumatra, the important land connectivity is between Medan City and Belawan Port. Belawan Port in Medan is currently the main international port supporting this maritime connectivity segment.

EC1 hosts some of the most agriculture-rich provinces in Southern Thailand that trade with Malaysia, Sumatra, and Singapore and participate significantly in the supply chain of goods traded outside the subregion. EC1 covers several provinces in the border areas of Malaysia and Thailand and anchors clustering major economic activities by developing industrial hubs and special economic zones. - EC2: The Straits of Malacca Economic Corridor

EC2 is a coastal corridor connecting Thailand’s southern provinces of Trang and Satun with Malaysia’s state of Perlis, and on to Port Klang, Penang, and Melaka along the western coast. Under the existing configuration, the EC2 maritime gateways are Tammalang Port (Satun), Port Klang (Selangor), Penang Port (Penang), and Tanjung Bruas Port (Melaka).

The approach to corridor connectivity is multimodal, with land and coastal linkages. Due to the proximity of this corridor to Sumatra, there is considerable potential to complement various production chain stages with the island, especially if a series of economic and industrial zones are established at strategic points along the corridor. This corridor has potential as a food hub, especially for halal products, since several food terminals and integrated food centers are being planned in the corridor. - EC 4: The Melaka-Dumai Economic Corridor

EC4 is a maritime corridor linking Riau Province in Sumatra to the state of Melaka in Peninsular Malaysia. The economic rationale underpinning this link is based on the strategic location of Dumai Port and Tanjung Bruas Port located opposite each other in one of the narrowest stretches of the Strait of Malacca, thus having the shortest cross-strait distance between them. The corridor includes enhancement of land connectivity to Dumai Port, as well as the creation of Tanjung Bruas Port. EC4 has a long tradition of freight and passenger traffic between Sumatra and Malaysia. Dumai is the gateway port of Riau Province, one of the richest provinces of Indonesia with abundant palm oil plantations and onshore oil and gas resources. Dumai is principally a palm oil-related export port with general cargo, fertilizer, cement, and rice as main import traffic. - EC 5: The Ranong-Phuket-Aceh Economic Corridor

EC5 is mainly a maritime corridor linking ports in the northern part of Sumatra (mainly Ulee Lheue and Malahayati in Aceh Province) with Southern Thailand along its western coast facing the Andaman Sea, with the aim of exploiting tourism potentials. In Sumatra, Aceh Province is part of the corridor and Banda Aceh, the capital, and Sabang (located in the adjacent We Island) are gateway and tourism nodes, respectively. EC5 is envisaged to enhance maritime connectivity between Sumatra and Southern Thailand by developing facilities in key ports of Sumatra (Figure 8) (Anwar, 2023).

2.4. International Economic Corridor Development

Malaysia-China Kuantan Industrial Park (MCKIP)

MCKIP was officially launched in 2013, and is strategically located in the ECER SEZ in Kuantan, Pahang. MCKIP is the key driver for attracting foreign investments to the industrial park. These investments promote job opportunities to locals and spur regional economic growth.

Launched in 2012, China-Malaysia Qinzhou Industrial Park (CMQIP) is the sister park to MCKIP in Qinzhou, China. Supported by China and Malaysia, CMQIP and MCKIP co-created a new Two Countries, Twin Parks model for international production capacity operations. Currently, it has 25 projects with RMB 5.3 billion total investment value.

Figure 9 Malaysia-China Kuantan Industrial Park (MCKIP)

Figure 10 Shipping Time between Kuantan Port and Qinzhou Port

3. Challenges to Economic Corridor Development in Malaysia

Malaysia’s economic corridors are strategic instruments for economic growth by attracting foreign investment into the national manufacturing sector. Spanning about 70 percent of Malaysia’s landmass, these corridors have drawn investments from major domestic and multinational companies. By 2023, the accumulated investment was estimated at over 700 billion ringgit (US$150 billion). The corridors aim to be hubs for high-tech industries such as semiconductors and establish the country as a key link in global supply chains (ASEAN Briefing Magazine, 2023).

Despite successful development, the economic corridors face several challenges:

3.1. Infrastructure Challenges

Generally, an EC is a collection of economic centres connected by land transport services, roads, railways and bridges. There are two types of infrastructure that directly affect corridor development: hard and soft infrastructures, correspondingly providing hard and soft connectivities. Hard connectivity includes physical infrastructure underpinning transport and communications services, while soft connectivity involves a skilled labour market, efficient digital infrastructure, and trade facilitation (Hill, 2020).

Portugal-Perez and Wilson (2012) underline that trade facilitation measures may be undertaken along two dimensions: a hard dimension related to tangible infrastructure such as roads, ports, highways, telecommunications, as well as a soft dimension related to transparency, customs management, the business environment, and other intangible institutional aspects.

3.1.1. Hard Infrastructure: Transport

Roads, railways, ports, airports and telecommunications that facilitate the movement of goods, services and people are categorised as hard infrastructure. It also includes efficient intermodal connections such as bridges connecting road networks, railways servicing ports, electronic communications, and physical connectivity operating together.

In Malaysia, infrastructure projects are significant strategic investments that act as key regional enablers by increasing connectivity and facilitating cross-border movement of goods and people to boost trade, business and investment. If connections weaken, international hubs operate as enclaves, resulting in rising urban-rural disparities and increased inequality. This challenge highlights the important role of economic corridors in facilitating connectivity and integration. Despite the recent accelerated growth of e-commerce, Malaysia still lacks key connectivity between ports and warehouses. Train lines, port facilities, effective technology and automation are not readily available nationwide. This is because the main objective of building economic corridors is to reduce regional imbalance and bring about equitable growth, investment and employment opportunities, and reduce poverty. By restructuring society, overall wealth creation may be accelerated to all regions of Malaysia. To achieve these objectives, economic corridors are designated in rural areas, where transport infrastructure development poses several challenges.

A lack of transport infrastructure, particularly the economic corridors in East Malaysia such as SDC and SCORE, is even more troublesome due to lack of basic infrastructure such as highways for carrying raw materials and extensive reliable electricity, indicating massive financial requirements for developing any large-scale project (Sovacool and Bulan, 2012).

Athukorala and Narayanan (2017) underline that infrastructure development involves revamping/developing transport routes that physically link areas/regions and establishing multimodal and intermodal transport facilities. To achieve the objective of integrating a designated region in the national economy and globally, it is important to prioritize developing a gateway as a focal point of the regionwide transport infrastructure.

A gateway is a metropolis with access through seaports, airports, and/or teleports to the rest of the world. A strategically located gateway fosters competitiveness of the economic corridor by reducing the trade cost of goods and service delivery. Much of the corridor-related policymaking and planning relating must develop gateway and corridor infrastructure to streamline interactions with global logistics service providers to interconnect local focus with global structure (Rimmer 2014).

Therefore, economic corridor success depends on establishing international gateway availability. Economic corridors lacking international air transport gateways such as ECER and major ports in East Malaysia will take longer to achieve success.

3.1.2. Other Facilities (Such as Dry Ports/Warehouses/DC/Fulfilment Centres)

Generally, seaport system complexity arises from changes in world trade development, supply chain and logistics tendencies, maritime transport advances, technological innovations, and interactions with different internal and external players (Cetin and Cerit, 2010; Jeevan et al, 2015).

In Malaysia, insufficient railway tracks have been a main challenge for Malaysian dry ports. The necessity for transferring containers from dry ports to seaports and vice versa requires rapid container clearance/movement to allocate more space for additional containers. Intense transport movement in one location may cause terminal congestion and spill over to surrounding regions. Issues of insufficient rail tracks or road use limitations affect the volume of containers handled by dry ports and dissuade potential customers from using facilities (Jeevan et al, 2015).

Likewise, inappropriate container movement operation planning may occur when schedules between container movement and arrangement on railway decks from dry port to seaports are unsynchronised, leading to delays in loading containers onto vessels. Unexpected delays in intermodal transportation and production as well as shortages in container handling equipment may also lead to an insufficient volume of containers loaded onto vessels and ultimately affect seaport competitiveness (Vernimmen et al., 2007).

The issue of non-strategic location of dry ports adjacent to seaports also affects the demand on the use of dry ports as it may be less expensive to bring containers directly to seaports and uneconomical for logistics companies to use dry ports. Therefore, the role of seaports in dominating hinterland regional markets has resulted in dry ports becoming competitors of seaports (Rodrigue et al., 2010). Locating dry ports far from manufacturing areas has also resulted in their closure. Traffic congestion in regional areas, lack of credibility of dry port operators and less potential for expansion are among other challenges faced by dry ports in Malaysia (Jeevan et al, 2015).

3.2. Soft Infrastructure: Institutional Challenges

Corridors are generally viewed by governments as a subset of spatial or regional policies, while public works and transport agencies are the governmental arms likeliest to be involved with them. For major projects, an interagency authority is often established (Athukorala and Narayanan, 2017). Improving access for the rest of the corridor to the gateway is a matter of building physical infrastructure as well as being accompanied by trade facilitation reforms. This involves harmonizing polices and regulations on the movement of people, freight, and related services, and improving the investment climate. Administrative procedures applying to goods in transit and key ancillary services, notably trucking, are also significant. Trade facilitation for logistics reforms is more important for cross-border economic corridors than cross-regional corridors in a given country.

Operationally, corridor development in Malaysia is private-sector driven and the government participates by providing a conducive environment for attracting private sector participation, such as competitive incentive packages as well as creating one-stop centres to enhance service delivery and promote investment. However, several issues remain:

3.2.1. Domestic Rules and Regulations

- Political Conflicts

Economic corridors are federal government initiatives for which statutory bodies, the NCIA, IRDA, ECERDC, SEDIA and RECODA, were created to oversee development and project implementation. The composition of the body with minimal participation of state-level officials poses potential coordination and implementation issues. For example, the NCER corridor model encompassing four states might encounter different views and development priorities. If all states were governed by the same political party, with similar or shared agendas, giving assistance and submitting information as detailed in section VII (C) of the Act may proceed smoothly. However, matters become more complicated when federal and state governments are controlled by rival parties (as in the case of Penang, a key state in the NCER) and where project priorities differ. This circumstance may not have been foreseen when the original blueprint was designed with Penang as regional integrated logistic hub of the NCER (Sime Darby 2007, Lim 2007). Clearly, the NCIA is either unable or unwilling to fully exert powers conferred upon it by the NCIA Act in dealing with an opposition-controlled state. By concentrating its efforts in the other three states, it may be following the path of least resistance. If so, the full benefits of complementarity between Penang and hinterland states may not be achieved.

Like other economic corridor authorities, the NCIA is basically a federal institution by design in which state governments and state-level stakeholders have limited roles to play, while all NCIA-implemented projects are federally funded on an individual basis. This vests an unwarranted amount of influence in federal hands and hinders the operational freedom of the NCIA. It is difficult for the NCIA to design policies and programs to resolve state development gaps and the rural–urban divide as envisaged in the original economic corridor proposal. This goal may only be accomplished by freeing the NCIA from excessive real and perceived federal control. If this issue is unaddressed, the NCIA will merely be an unnecessary institution that duplicates what may already be done by individual states (Athukorala and Narayanan 2017). Similar situations may recur in other economic corridors. - Land acquisition issues

In the Malaysian version of the federal system, the most important powers remain with the federal government (Hutchinson 2015). By contrast, the states have sole jurisdiction over land matters within their boundaries, useful only for determining the location of investments and other infrastructural development. Land acquisition issues may present a major obstacle to major corridor projects, which invariably require greenfield sites. This is a particular problem in densely settled countries with poorly developed land titling, and where past acquisition practices have resulted in unresolved grievances.

For example, Kedah’s manufacturing sector has attracted RM1.5-RM2.2 billion in annual investment from 2016 to 2018. While this investment figure exceeds that of Perak and Perlis, Kedah has potential to attract even more investment, and capture the spillover from Pulau Pinang. But Kedah is facing challenges in terms of land availability because a significant portion (76%) is classified as Malay Reserve Land, which makes it difficult to attract investors because of restrictions and bankability (NCER, 2020).

3.2.2. Regional rules and regulations

IMT-GT and BIMP-EAGA have been the focused regional economic corridors in Malaysia. Policy directions have been updated in the Five-Year Malaysia Plan, the Master Plan of each economic corridor, and the Industrial Master Plan.

Challenges of rules and regulations in each master plan usually relates to technical matters such as:

- Complicated, unstandardized, and unharmonized cross-border formalities, procedures, and rules governing movement of road vehicles.

This includes customs, immigration, and quarantine (CIQ) rules, regulations, and procedures governing admission of foreign commercial and private vehicles and cargo and passengers in the vehicles. - Practical challenges with respect to mutual recognition of vehicle inspection certificates, insurance policies, vehicle registrations, and cross-border vehicle permits.

For example, under the IMT-GT, the planned Ro-Ro ferry link between Dumai and Melaka has yet to materialize because outstanding physical infrastructure and regulatory issues must be resolved related to the aforementioned matters.

The Melaka–Dumai Ro-Ro Ferry Project, planned under the IMT-GT IB 2012–2016 and continued under IB 2017–2021, involves Tanjung Bruas Port in Melaka and Sri Junjungan Port in Riau. This route has been identified to serve as a main trade gateway. It is expected that both port authorities will build their respective Ro-Ro terminal facilities and this project will facilitate cargo shipment between Melaka and Dumai by using lorries transported on Ro-Ro ferries. This facility may reduce travel time from one week to only five hours to cross the Straits of Malacca when the process of loading and unloading at ports is no longer necessary. Maritime trade activity between Malaysia and Sumatra will likely be enhanced due to reduced travel time.

However, still being deliberated are technical specifications of vehicles that will enter or exit ports and cross border areas (Anuar, 2023).

3.3. Logistics Service provider challenges

Generally, Malaysia’s logistics market is dynamic, with opportunities for growth across diverse sectors. The industry continues to evolve, adapting to changing demands and technological advancements (Pwc, 2018) with strong growth enablers such as improvements in logistics infrastructure, rising freight volumes, the rise of e-commerce, and expansion of the manufacturing sector. The market size is estimated at USD 28.12 billion in 2024 and is projected to reach USD 38.28 billion by 2030, growing at a compound annual growth rate (CAGR) of 5.28% from 2024 to 2030. Key segments include end-user industries such as agriculture, construction, manufacturing, oil and gas, mining, and wholesale and retail trade, as well as courier, express, and parcel (CEP) logistics companies, freight forwarding, freight transport, and warehousing. Niche segments, particularly cold chain logistics, are attracting interest due to healthy margins and increasing demand for perishable goods. Notably, the manufacturing sector holds the largest share in the market, contributing 39.34% (Mordor Intelligence, 2024).

Despite pandemic-related challenges, the logistics industry in Malaysia remains resilient. The nation’s primary air cargo players are actively expanding operations, with My Jet Xpress and World Cargo Airline enhancing services. The domestic CEP market is poised for growth due to increasing e-commerce user penetration, projected to reach 55% by 2030. The warehousing market is also thriving, driven by rapid e-commerce growth and over 1,000 companies involved in delivering e-commerce shipments nationwide. Revenue-generating sectors for the logistics market include food and beverage (F&B), manufacturing, electronics, automotive, and pharmaceuticals.

Despite the strong growth of the logistics sectors, industrial concentration is mainly on the west coast of Peninsular Malaysia, with almost 70% located in the northern and southern regions of Klang Valley. A key challenge faced by the ECER manufacturing cluster is limited logistics and accessibility. The lack of an international gateway has caused ECER to focus more on domestic trade as well as cross-border trade with Thailand.

Another challenge faced by the economic corridor is dominance by large foreign corporations. For example, in the East Coast Economic Region (ECER), the oil, gas and petrochemical (OGP), sector, a major economic contributor, has been affected by the presence of multinational companies. The absence of industry 4.0 adoption among local companies using big data-driven quality control, information and communication technology (ICT)-based systems, predictive maintenance, and machine-to-machine communication has exacerbated this issue.

3.4. Manufacturing, Trading, and Investing challenges

The manufacturing sector has been a key economic motivator in all economic corridor regions. The greenfield and resource-rich ECER contributes to the bulk of private regional investment, creating a major spillover effect for societal benefit. This sector is expected to remain an economic backbone, while the West Coast states (NCER) move towards a service-based economy. In line with the Government’s Third Industrial Masterplan (IMP3), ECERDC has established 12 thematic industrial parks regionally for targeted industries equipped with infrastructure needed to provide a conducive investing environment (ECER, 2019)

Manufacturers faced several key challenges related to being situated in rural areas. Attracting private investment has been a core challenge for economic corridors, especially those lacking transport infrastructure: ECER in the east coast, SDC and SCORE in East Malaysia. Absence of transport infrastructure has led to regional limitations in logistics and accessibility (ECER, 2019).

Human resources is another challenge faced by manufacturers, traders and investors. Human capital is a critical element for growth and development to support regional industrial foundation.

For generations, agriculture has traditionally been the mainstay of economic regions, and remains a focal area in economic corridors, but significant issues and challenges remain that prevent the sector from achieving higher value-added contribution to the economy: low productivity, aging farmers, high production costs, outdated technology, limited financial resources, and unskilled workers. Consequently, the focus is to transform traditionally small-scale farms into large-scale, commercial agribusiness ventures.

4. Overcoming Economic Corridor Development Challenges

The economic corridor is expected to create new sources of growth and ensure more coordinated, integrated, widespread, and comprehensive economic development. Additional regional income will be generated to accelerate poverty eradication, societal restructuring, and overall wealth creation. The creation of regional corridor authorities will spearhead efforts to facilitate and expedite implementation of programmes and projects identified in a master plan for each growth corridor. Malaysia has initiated several approaches to overcoming economic corridor challenges.

Collaboration between the federal government and state governments will be strengthened to promote cross-regional sustainable and balanced development. The role of key state level agencies will also be streamlined to support more effective regional planning and coordination. This will involve rationalising the role of all state economic development corporations (SEDCs), state economic planning units, regional development authorities and regional economic corridor authorities. State governments development plans will be streamlined to support and complement federal development policies and strategies. State policy, such as the Smart Selangor Action Plan 2025, Pelan Induk Terengganu Sejahtera 2030, and Perlis Digital Plan 2021-2025 will be aligned to national digital transformation objectives. State initiatives, such as the improvement of logistics services, river management, and aerospace industry growth will be mapped with the respective development policies at the federal level. These alignments will facilitate better development planning to achieve more balanced regional growth. (Twelfth Malaysia Plan, 2020 p.6-17).

The private sector drives corridor development through a cluster approach, franchise and vendor programmes, and by facilitating entrepreneur participation in regional corridors and new growth areas. Private sector participation is essential for driving growth corridor development, and the Government duly promotes a more conducive environment to attract greater private sector participation. (RMK 9, 2006). The nodes/cluster/zones approach has also enabled optimisation of Government resources to reach the population and key economic activities (NCER, p 29). The strategy will address a key challenge faced by economic corridors: how to attract private investment that will enable greater job creation and entrepreneurial opportunities, generating household income for communities. Incremental household income may sustain industry interest and attract sufficient workers to counter the outmigration of talent in recent years (NCER, 2019)

An anchor company business model for agribusiness projects has also been introduced in NCER. For example, serving as a nuclear farm providing technical training to satellite farms, improving processes, and using strategic inputs to move farming activity up the value chain. This business model aims to address challenges by promoting competitive, sustainable industry, bridging gaps in the value chain and creating high-income farmers (NCIA). Driven by the private sector, the anchor company model is aligned to the National Food Policy – Direction 2019-2020. The anchor companies are selected as mentors based on their existing track record, readiness, and approval from the State Steering Committee (JPN). The model focuses on high-value products such as superfruits, oysters, organic rice, cash crops, and aquaculture. Another opportunity arising from agribusiness is agrotourism, which can create potential spillover benefits to the local economy by generating a need for accommodation, food and beverage, and transportation services.

Human capital development programmes were designed to address regional challenges, including low household income, less-than-optimal labour force participation, and high graduate unemployment rates. Diverse initiatives have been introduced to address these challenges and develop local regional talents inclusively and holistically (ECER, 2019) to benefit over 10,000 local residents. Human capital development must continue to be a key priority, so corridor authorities bridge existing skills gaps in the labour market through different interventions and initiatives, including reforming the labour market and prioritising skilled job creation, improving work efficiency and productivity, enhancing access to quality education, and training and fostering stronger industry-academia links. Entrepreneurship will continue to provide additional community income as a growth engine in rural areas (NCER, 2019, p.57).

Simultaneously, economic enablers such as enhanced strategic logistics, transportation and utilities infrastructure will also be introduced to strengthen rural-urban linkages. Transport infrastructure projects are being developed to enhance regional last mile connectivity for goods and services. For example, in the ECER, the ECRL, Kuantan Port expansion, Central Spine Road, and Machang-Pasir Puteh-Tok Bali Link will also unlock new economic opportunities in areas that were previously inaccessible. In this way, new industrial parks will be established through private sector investment. An effective logistics system will further stimulate trade, enhance business efficiency, and spur economic growth across all economic sectors. Facilitation of seamless movement of goods and services across the region will benefit other economic clusters as well as local entrepreneurs who may access the regional marketplace more easily. From a wider perspective, the sector will be an essential link for more effective trading between ECER and the West Coast of Peninsular Malaysia, as well as Asia Pacific markets, in line with ECER’s aspiration to become the Gateway to Asia Pacific (ECER, 2019). Introducing the logistics and services cluster into the ECER as a new key motivator will enhance regional competitiveness by identifying, aggregating, and addressing cross-sector supply chain issues, particularly in the agribusiness, oil, gas and petrochemical, manufacturing, and tourism clusters. In addition, supply chain-related issues in ECER’s manufacturing sector will be addressed.

Nevertheless, the robust extant NCER logistics and transportation infrastructure strengthens urban rural linkages and enhances regional connectivity and mobility. The logistics sector is a key trade enabler for NCER, along with the established cluster of support services and well-developed gateway. The thoroughly planned and expertly constructed infrastructure network are a supportive ecosystem necessary for economic expansion, promoting inclusivity, and raising living standards. Under the NCER Strategic Development Framework (2021-2025), NCER infrastructure will be strengthened by three strategies:

- Improved logistics, transportation and utilities infrastructure

- Strengthened urban-rural links

- Strengthened connectivity and mobility

The strategic positioning of NCER and IM along the major maritime trade route and a main Malaysian international import and export gateways benefits both regions. As of 2018, NCER handled over 45% of Malaysia’s manufacturing exports, and Penang International Airport managed almost double the value of goods handled by KLIA. In addition, the reliance of Southern Thailand cargo on NCER export and import points has made Bukit Kayu Hitam and Padang Besar major gateways for over 67% of Southern Thailand exports, or about 250,000 twenty-foot equivalent units (TEUs). Developing logistics and connectivity means 1) resolving bottleneck congestion at borders; 2) facilitating private investment; 3) improving growth node area logistics; and 4) regionalizing logistics and trade facilitation master planning.

5. Summary

Over the past two decades, economic corridors have gained popularity as vehicles for subregional economic development and potential for promoting equitable growth among regions sharing international borders, as well as in areas within national borders with significant income disparities. In Malaysia, the concept of regional development began in 1970 after 13th May 1969 race riots sparked by uneven regional development, political instability, racial issues, and diverse aspects of disparity. This incident became an impetus for developing the National Economic Policy (1970-1990) and New Development Policy (1991-2000), which guided regional development implementation. The nationwide five economic corridors were introduced in the Ninth Malaysia Plan (2006-2010). The Tenth Plan became operational around 2006-2008 and will end between 2025 and 2030.

During 18 years of economic corridor foundation, significant progress has been made in regional economic development. Significant community employment opportunities have been provided, new manufacturing clusters developed, logistics and infrastructure improved and investment opportunities offered to foreign businesses in sectors that have transformed the nation into a leading Southeast Asian economic power. Emergent specialised sectors include oil and gas, manufacturing, agriculture, logistics, tourism, and biotechnology. A well-educated workforce, good infrastructure, and business-friendly policies have turned Malaysia into a reliable investment destination.

Despite successful economic corridor growth, development speed has varied according to economic corridor. Those equipped with better hard and soft infrastructure as well as international gateway availability, like NCER, tends to grow faster than those lacking this infrastructure, especially the SDC and SCORE in East Malaysia. Spatial areas designated for development under both agencies are relatively large, while the scope of economic activities is wide-ranging, without area focus where states might have potential and comparative advantages.

Attracting investment has been challenging in all economic corridors, especially for Sabah and Sarawak to interest other regions and other Brunei Darussalam–Indonesia–Malaysia–Philippines East ASEAN Growth Area (BIMP-EAGA) members. The relatively higher cost of doing business in the two states also serves as an investment deterrent. Therefore, they have yet to achieve the intended outcomes.

Imbalanced urban development across areas remains an issue. A lack of data integration as well as ineffective coordination between state and federal agencies have resulted in fragmented development planning and monitoring. Private sector participation, including social enterprises in rural area economic activities, remains relatively low, especially in the East Malaysia. This is due to insufficient basic infrastructure and logistics services, contributing to an absence of employment and economic opportunities in rural areas. Despite several obstacles to corridor development, the nation is gaining increased importance in global supply chains, particularly due to trade tensions between the US and China. One example is as a location for semiconductor producers looking to diversify business risks. In addition, Malaysia has a well-established industrial sector, presenting opportunities in manufacturing, medical devices and tourism, healthcare, semiconductor and electrical and electronic (E&E), the digital economy, the halal industry, and Islamic finance (ASEAN Briefing, 2023). Still, much remains to be done to accelerate economic corridor success.

Refferences

- Alhabshi, S.M. (2011), E-Government in Malaysia: Barriers and Progress, in The Handbook of Research on Information Communication Technology Policy: Trends, Issues and Advancements, DOI: 10.4018/978-1-61520-847-0.ch009, p.121-146.

- Anuar, A.R. (2023) Review and Assessment of the Indonesia-Malaysia-Thailand Growth Triangle Economic Corridors: Malaysia Country Report, Asian Development Bank, March.

- ASEAN Briefing Magazine (2021), An Overview of Malaysia’s Investment Corridors, Asia Briefing Publication Store, April 9.

- ASEAN Briefing Magazine (2024), Singapore and Malaysia Plan Joint Special Economic Zone in Johor State, Asia Briefing Publication Store, January 18.

- ASEAN Briefing, Promising Sectors for Investments in Malaysia’s Economic Corridors, December 27, 2023, https://www.aseanbriefing.com/news/promising-sectors-for-investments-in-malaysias-economic-corridors/, accessed at 30 march 2024.

- ASEAN Briefing Magazine (2023), Malaysia’s Economic Corridors: A Guide for Foreign Investors, Asia Briefing Publication Store, December 2.

- Athukorala, P. and Narayanan, S. (2018), Economic Corridors and Regional Development: The Malaysian Experience, ADB Working Paper Series (No.520), December, DOI: http//dx.doi.org/10.22617/WPS189287-2.

- Athukorala, P. and Narayanan, S. (2018), Economic Corridors and Regional Development: The Malaysian Experience, World Development, Issue 106, pp. 1-14.

- Cetin, C.K. and Cerit, A.G. (2010), Organisational Effectiveness at Seaports: A system Approach, Maritime Policy and Management, Vol.37, No.3, pp. 195-219.

- East Asia Forum (2024), Malaysia must take bold economic action, accessed at https://eastasiaforum.org/2024/02/13/malaysia-must-take-bold-economic-action/#:~:text=The%20Malaysian%20economy%20has%20proved,the%20second%20quarter%20of%202023. February 13.

- East Coast Economic Region Development Council (ECERDC), (2019), ECER Master Plam: The Next Leap (2018-2025), ECERDC, 1 October.

- Hill, H. and Menon, J (2020) Economic Corridors in Southeast Asia: Success Factors, Impacts and Policy, Economics Working Paper No. 2020 – 03, Yusof Ishak Institute, pp.1-28.

- Jeevan, J., Chen, S. and Lee, E. (2015) The Challenges of Malaysian Dry Ports Development, The Asian Journal of Shipping and Logistics, Vol. 31 No.1, March, pp. 109-134.

- MIDA (XXXX), Chuping Valley Industrial Area: The Premium Border Town Technology Park for Investors, accessed at https://www.mida.gov.my/chuping-valley-industrial-area-the-premium-border-town-technology-park-for-investors/ on 31 March.

- Ngah, I. (2011), Overview of Regional Development in Malaysia, presented to the International Conference on Regional Development, Vulnerability, Resilience and Sustainability, 9-10 November.

- Northern Corridor Implementation Agency (2020) Northern Corridor Economic Region Strategic Development Plan (2021-2025), NCIA, Pulau Pinang, Malaysia.

- Portugal-Perez, A. and Wilson, J.S. (2012), Export Performance and Trade Facilitation Reform: Hard and Soft Infrastructure, World Development, Vol. 40, No. 7, pp. 1295–1307.

- PWC (2018), Logistics in Malaysia Market overview and M&A trends, accessed at https://www.pwc.com/my/en/assets/blog/pwc-my-deals-strategy-logistics-in-malaysia.pdf

- The Malaysian Reserve (2023), Malaysia’s economy grapples with export slowdown, global challenges, accessed at https://themalaysianreserve.com/2023/07/03/report-malaysias-economy-grapples-with-export-slowdown-global-challenges/ , July 3.

- The World Bank (2022), Overview of Malaysia, accessed at https://www.worldbank.org/en/country/malaysia/overview , November 29.

- Sovacool, B.K. and Bulan, L.C. (2012), Energy Security and Hyropower Development in Malaysia: The Drivers and Challenges facing the Sarawak Corridor of Renewwable Energy (SCORE), Renewable Energy 40, pp. 113-129.